26

Jan

Four years of dedicated work have finished!

PrimeFish (2015-2019) has wrapped after 4 years of research in the European seafood market. Thanks to the dedicated work of the consortia members and ... read more

The EU is the largest market in the world for fish; with a value of €55 billion and a volume of 12 million tons. While EU seafood consumption has risen over the past 10 years with stable or declining supply from the fisheries sector, most of this increase has come from imports rather than from EU aquaculture. Today 25% of all EU seafood consumption comes from EU fisheries, 10% from EU aquaculture and 65% from imports from third countries, both fisheries and aquaculture products. European aquaculture growth has stagnated since the turn of the century partly because its products have not been competitive compared with imports.

Catch volume, aquaculture production volume and market prices have varied a lot over time, and this has had severe effects on profitability in different seafood sectors and for different product types, leading to numerous seafood company bankruptcies. In addition the seafood sector, especially the captured fish sector, is in some countries expected to provide value to the society beyond company profit, in particular in relation to employment for fishermen and for the processing industry in rural areas. These additional expectations, coupled with unique requirements for sustainable harvest and production, make it difficult to achieve stable profit over time for a seafood company. The captured fish industry has its main challenges related to the supply of fish, both because of overfished stocks and because of the extreme seasonality for main species. This in turn leads to market-related challenges for captured fish, as it may be more profitable to catch less fish when the price is high. The European farmed fish industry has its main challenges on regulatory issues, conflicts with other water users, but also directly related to the market and to the lead time in the production cycle (for a temperate specie, such as salmon typically 24-36 months). With price per kg for salmon varying from around €2 to well over €5 (since 2000), it is very difficult to assess the expected profitability of different business cases. A well-known problem, particularly in the sea-bass and sea-bream industry and up until quite recently also in the salmon industry, is the “boom and bust” cycle. This is when high prices in the market encourage individual companies to increase production significantly (boom). However, when all companies react in this manner the market is flooded, leading to overproduction, low prices, declining profits and eventually bankruptcies (bust).

These severe and to some degree unique challenges lead to various societal problems in relation to the seafood industry. This is a RTD project called “Developing Innovative Market Orientated Prediction Toolbox to Strengthen the Economic Sustainability and Competitiveness of European Seafood on Local and Global markets” or PrimeFish where an attempt is made to address some of these challenges.

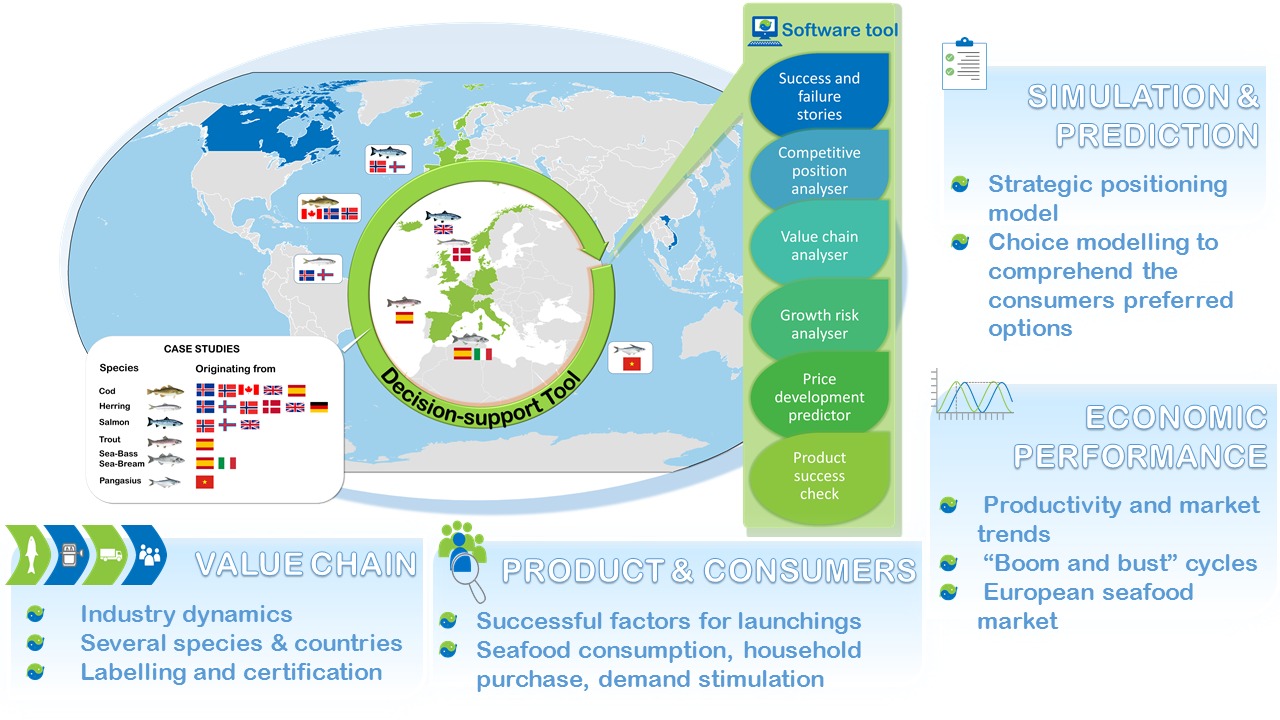

Here you can find out more about the activities developed in the frame of PrimeFish as well as the more interesting results for the Seafood companies.

PrimeFish (2015-2019) has wrapped after 4 years of research in the European seafood market. Thanks to the dedicated work of the consortia members and ... read more

PrimeFish DSS is a webtool for fishermen, aquaculture producers, processing companies, market analysts, public authorities and other stakeholders. It ... read more

Access here the main outputs developped by the H2020 project PrimeFish (2015-2019) for the seafood industry: - The market intelligence tool PrimeDSS M... read more